A REVERSE MORTGAGE ON AMERICA

In 2010 we published a KnowRisk Commentary with a greatly simplified description of the US budget called Federal Budget 101. Since the same issue has not only remained, but unfortunately grown in size, we thought it timely to revisit the Jones family and see how they are progressing in a new article called A Reverse Mortgage on the Country.

Years ago, I published this analysis of the government debt and deficit. The numbers are so large, in order to make it more understandable I knocked off 8 digits to create the parallel to a family household called the “Jones family”. Apparently, no one from the government read the publication because the Jones family scenario has grown worse. Today we will update the numbers. Let’s put the federal budget into perspective. The 2023 fiscal year Federal Budget analyzed in simple terms:

- U.S. Income: $4,440,000,000,000[i]

- Federal Budget: $6,130,000,000,000i

- New Debt: $1,700,000,000,000i

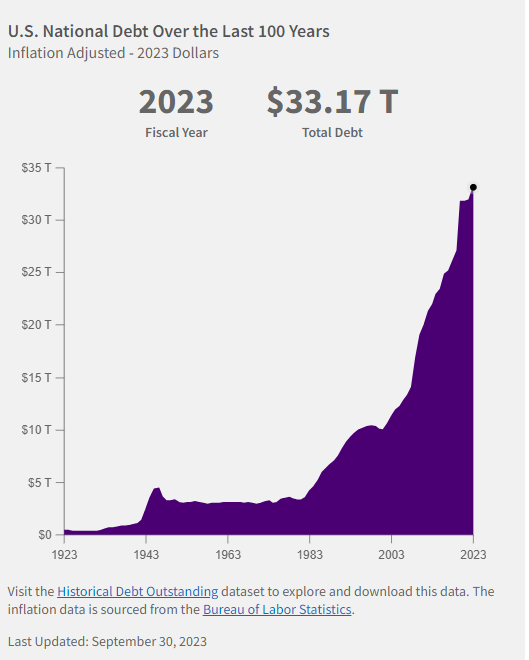

- National Debt: $33,170,000,000,000i

- Deficit Spending: 27.7% (% of all Spending)

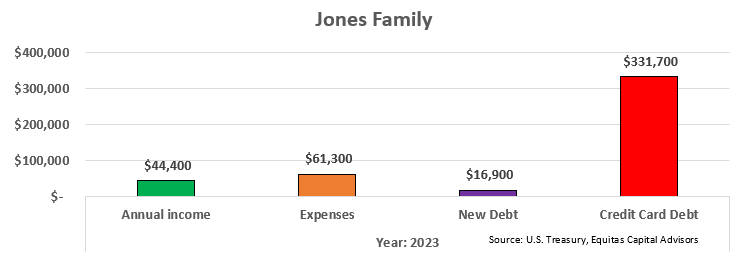

It helps to think about these numbers in terms that we can relate to. Let’s remove eight zeros from these numbers and pretend this is the household budget for the fictitious Jones family.

- Annual Income: $44,400

- Expenses: $61,300

- New Debt: $16,900

- Credit Card Debt: $331,700

- New Debt/Expenses: 27.6%

At the end of the 2023 fiscal year, the federal government had an average interest rate of 2.97%.ii This number is increasing rapidly with the interest rate from a 1-month T-Bill at 5.355% as of this letter.iii If all of our debt had this interest rate, our annual interest payments would be 40% of our yearly revenue. This is, still, substantially lower than what the Jones family would pay thanks to interest on Federal Debt being much lower than most individuals’ debt. As of November 2023, the average APR for an individual’s debt is 22.75%.iv This would amount to $75,462 a year in interest payments for the Jones family. That’s 170% of their annual income! If they used all of their income to pay off their interest, they’d still have $31,062 left in annual debt payments. They wouldn’t have any money for basic living expenses such as for groceries, rent, utilities, etc.

In 1945, just after World War II, the Jones family’s debt stood at $43,800.i At the end of 1983, their debt was $42,000.i In 38 years, their debt actually fell $1,800. The Jones family practiced fiscal responsibility and demonstrated their ability to run a surplus. In the next 38 years, their debt rose $275,900i. Their debt’s exponential growth is a ticking time bomb.

Currently, the market is anticipating a soft landing with lower interest rates. If this is incorrect, it would only exasperate the fiscal burden. The higher the interest rates, the more costly the debt.

One option to combat this debt is inflation. This is an option for the government, but this is not an option for the Jones family. The debt is denominated in US dollars, and if the dollar lessens in value, so does the debt. Unfortunately, this would erode the purchasing power of consumers and corporations and pose challenges to economic stability and growth.

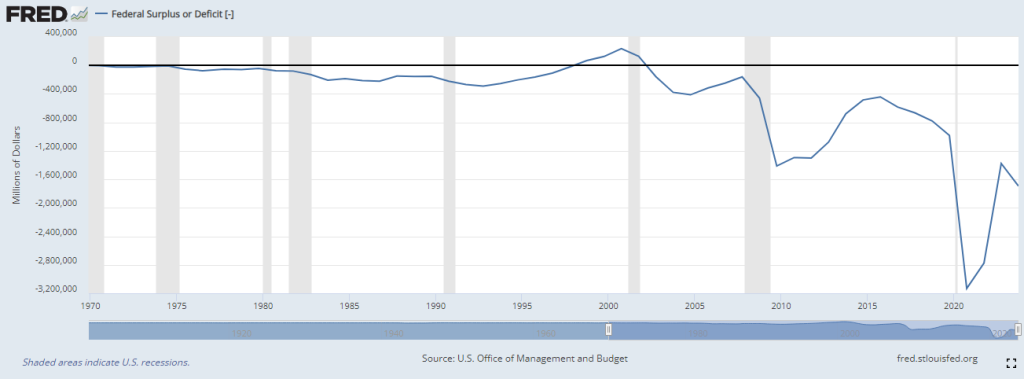

Now after years of irresponsible decisions, the Jones family has $331,700 of debt on its credit card (which is the equivalent of the national debt). That’s 7.47 years of their annual income, and they continue to add to their debt year after year. They haven’t had a surplus since 2001. Since that time, their debt skyrocketed by $231,800.i That is almost 70% of their total debt! One would think the Jones family would recognize and address this situation, but they do not. Neither does Congress.

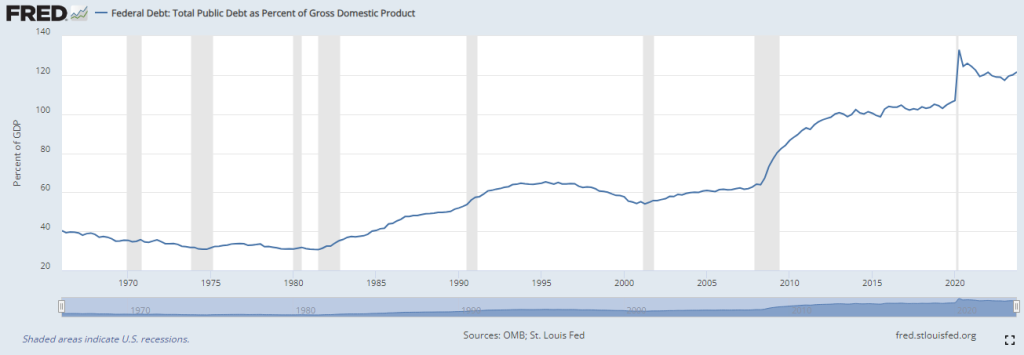

Essentially, what we have is a reverse mortgage on the country, a practice where we draw upon future resources to meet present demands. To date, total Debt-to-GDP has reached 120%. This is important to note, especially in light of a 2010 World Bank study that suggested a ratio greater than 77% had a negative impact on real growth levels. Another study from Penn-Wharton Budget Model suggests that 200% would be a maximum limit for U.S. debt held by the public.

Lower interest rates will help narrow the deficit, but more work is needed if Congress hopes to normalize our debt levels. A reduction in Federal spending, or an increase in revenue (taxes) has the potential for a cooling effect on both the economy and inflation. Under an ideal scenario, the deficit shrinks together with inflation and interest rates, bringing us into a smooth landing. Equitas Capital Advisors is watching for any unexpected developments, and ready to react if necessary.

In 2002, Equitas Capital Advisors, LLC was established as a unique company that blends the resources of a large global corporation with the flexibility of a small boutique firm. The registered service mark of Equitas Capital Advisors is Engineering Financial Solutions®and the purpose of Equitas is to design, build, and deliver investment solutions to meet the goals and objectives of our investors. Equitas Capital Advisors, LLC located in New Orleans, has over 200 years of combined investment management consulting experience providing professional investment management services to investors such as foundations, endowments, insurance companies, oil companies, universities, corporate retirement plans, and high net worth family offices.

Disclosures and Disclaimers:

Above information is for illustrative purposes only and has been obtained from reliable sources but no guarantee is made with regard to accuracy or completeness. It is not an offer to sell or solicitation to buy any security. The specific securities used are for illustrative purposes only and not a recommendation or solicitation to purchase or sell any individual security.

Equitas Capital Advisors, LLC is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the advisor has attained a particular level of skill or ability.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author on the date of publication and are subject to change. This publication does not involve the rendering of personalized investment advice.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment or strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor. Charts and references to returns do not represent the performance achieved by Equitas Capital Advisors, LLC, or any of its clients.

Asset allocation and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment losses. All investment strategies have the potential for profit or loss. There can be no assurances that an investor’s portfolio will match or outperform any particular benchmark.

i “Fiscal Data Explains the National Deficit.” | U.S. Treasury Fiscal Data, fiscaldata.treasury.gov/americas-financeguide/

ii Published by Statista Research Department. “Monthly Interest Rate U.S. Debt 2024.” Statista, 12 Mar. 2024,

www.statista.com/statistics/1382455/monthly-interest-rate-usdebt/#:~:

text=As%20of%20February%202024%2C%20the,reached%2034.47%20trillion%20U.S.%20dollar.

iii “TMUBMUSD01Y | U.S. 1 Year Treasury Bill Overview | Marketwatch.” Market Watch,

www.marketwatch.com/investing/bond/tmubmusd01y?countrycode=bx. Accessed 10 Apr. 2024.

iv Pincus, Melanie. “What Is the Average Credit Card Apr?” CNN, Cable News Network, 21 Feb. 2024,

www.cnn.com/cnn-underscored/money/average-credit-cardapr#:~:

text=The%20average%20annual%20percentage%20rate,when%20you%20open%20a%20card.