MASTERING FEAR AND GREED

Warren Buffett once highlighted a peculiar characteristic of human nature:

“Pension Funds in 1970 put 100% of new money into stocks because they were wild about stock. Then stocks got a lot cheaper in 1978 and they put a record low of 9% of new money into stocks. People behave very peculiarly in terms of their reactions because they are human beings. They get excited when others are excited. They get greedy when others are greedy. They get fearful when others are fearful, and will continue to do so. You will see things you will not believe in your lifetime in the securities market. The country will do very well over time, but you will see these huge waves. If you can stay objective and detach yourself temporarily from the crowd, you can get very rich”.

Newton’s first law of motion states that an object in motion will remain in motion unless acted upon by an outside force. This tendency to resist changes in motion is known as inertia. This concept also applies to the patterns of human behavior when investing. When stock prices decline, stress levels rise, increasing the emotional urge to sell. Conversely, as investment values increase, so does euphoria, strengthening the desire to buy. This leads to the common tendency to buy high and sell low, the opposite of successful investing.

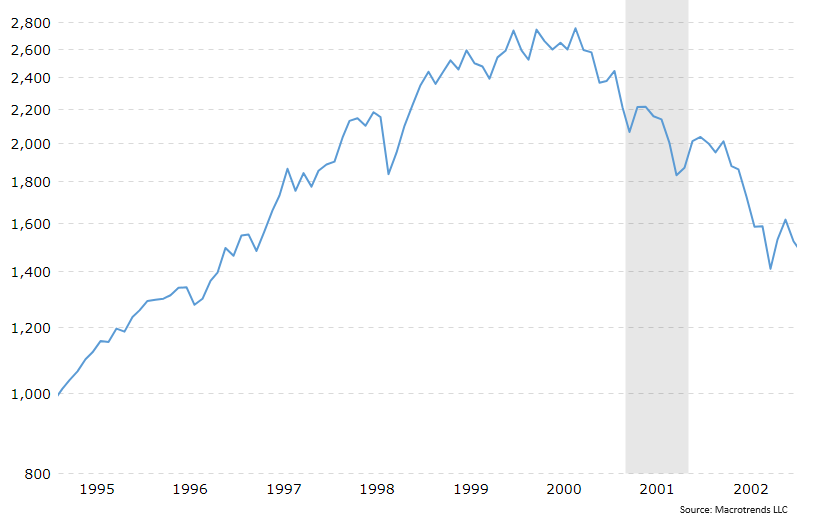

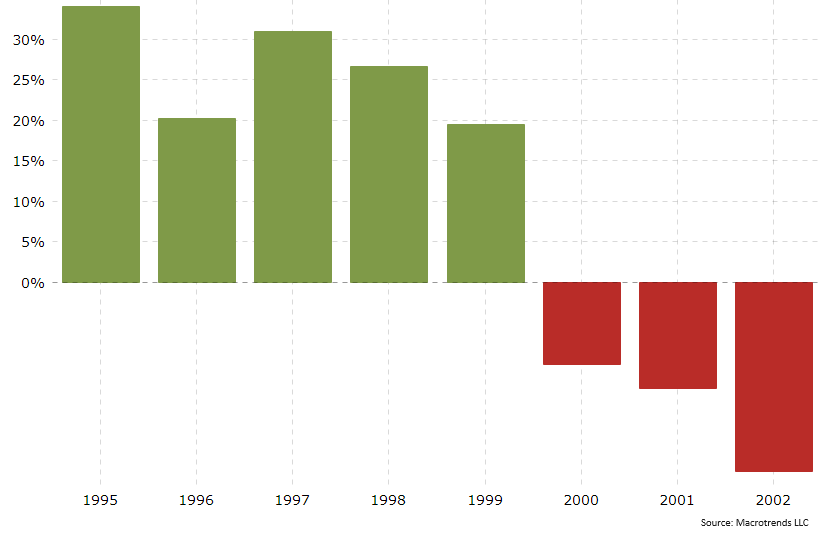

Let’s examine a historical scenario for more context. On the next page is a graph of the S&P 500 from 1995 to 2002. From the beginning of 1995 to the beginning of 2000 the index price increased from about 20% to 35% each year. Every year it felt like the market moved from fairly valued, to overvalued, to highly valued, to irrational exuberance. Selling in the early years would have missed the full increase and been judged poorly. However, going into the year 2000, the momentum shifted. Right then, a sale was the best option before the S&P 500 lost half its value, and the NASDAQ lost 80%, by 2002.

This is a good example of a technical market correction. Did the companies of the S&P 500 lose half their intrinsic value in 2002? No. Were the companies worth the high price set in 1999? Again, the answer is no. The market overshoots in wide swings above and below its fundamental value. These are the technical swings of the market caused by human behavior. Over the short term, these technical swings are as powerful for stocks as duration is for bonds. No one can predict or time these market shifts, but market sentiment and momentum can be tracked, measured, and analyzed.

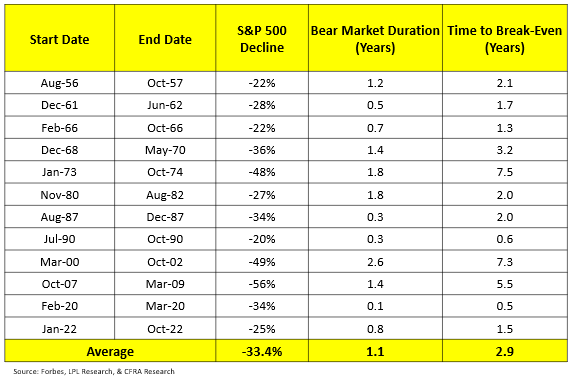

The table below shows all the S&P 500 bear markets since inception of the index. The average loss is over 33%, the average bear market duration is over a year, and the time to break-even is just under 3 years! Sometimes it is as long as 7 years.

So, when should stocks be sold, and when should the winners be allowed to run? As we discussed in our April 2024 bond seminar, despite 8.5% bond yields, equity market prices have increased from high to even higher. Rebalancing out of growth early would have been a mistake.

Many investors cannot handle the downturns and delays of these market cycles. Many on-profit institutions, like University Endowments or other Foundations for example, need cash flow for their mandatory spending every semester. Retired individuals need regular cash flow for living expenses. By analyzing the technical indicators, some risk management can be brought in that does not exist with purely fundamental analysis of index funds. Passive index funds are built on the fundamental size of the stocks in the index, and must remain fully invested at all times due to their prospectus. By combining technical and fundamental research, we find risk management characteristics that are otherwise absent in index funds.

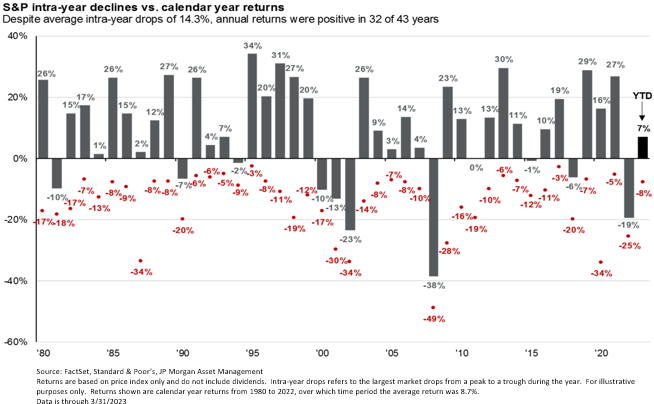

Embedded in each year’s stock market return is a drawdown shown in red below. The “average investor” tends to get uncomfortable and can sell at these bottoms. Risk management is needed to protect against this emotional human behavior.

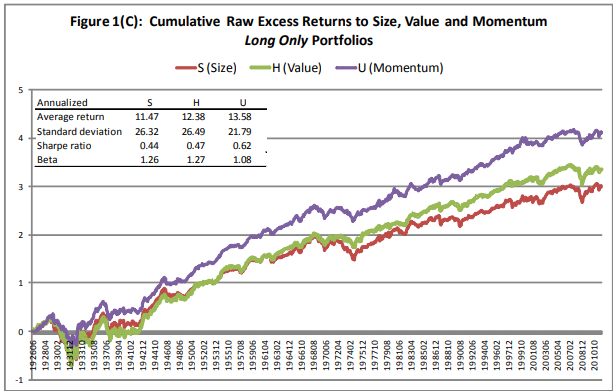

Momentum and technical analysis has been well-studied, with many papers indicating a significant market edge. In 2012, researchers Ronen Israel and Tobias Moskowitz demonstrated that Momentum has historically outperformed both Size and Value factor investing from Fama French:

Several professional research companies have performed similar and expanded studies with published calls going back decades. After our in-depth review of their work, Equitas now works directly with these researchers. This dimension of analysis is currently at work for many of our client portfolios. We welcome you to contact us today to learn how these tools can serve a valuable function in your portfolio.

Warren Buffett trained himself to not be worried about the wide market swings of his stock portfolio and looked beyond the market value to the value of the underlying businesses. This worked very well for him; however, the volatility of those market swings caused him to lose half his net worth 5 times in his career! 3 of those were with Berkshire Hathaway stock. Mr. Buffett is the only man I ever met who can take that kind of risk without becoming very emotional and irrational. For the rest of us, we need the safety and risk management of technical analysis.

In 2002, Equitas Capital Advisors, LLC was established as a unique company that blends the resources of a large global corporation with the flexibility of a small boutique firm. The registered service mark of Equitas Capital Advisors is Engineering Financial Solutions®and the purpose of Equitas is to design, build, and deliver investment solutions to meet the goals and objectives of our investors. Equitas Capital Advisors, LLC located in New Orleans, has over 200 years of combined investment management consulting experience providing professional investment management services to investors such as foundations, endowments, insurance companies, oil companies, universities, corporate retirement plans, and high net worth family offices.

Disclosures and Disclaimers:

Above information is for illustrative purposes only and has been obtained from reliable sources but no guarantee is made with regard to accuracy or completeness. It is not an offer to sell or solicitation to buy any security. The specific securities used are for illustrative purposes only and not a recommendation or solicitation to purchase or sell any individual security.

Equitas Capital Advisors, LLC is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the advisor has attained a particular level of skill or ability.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author on the date of publication and are subject to change. This publication does not involve the rendering of personalized investment advice.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment or strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor. Charts and references to returns do not represent the performance achieved by Equitas Capital Advisors, LLC, or any of its clients.

Asset allocation, momentum analysis and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment losses. All investment strategies have the potential for profit or loss. There can be no assurances that an investor’s portfolio will match or outperform any particular benchmark.