Trees Do Not Grow to Space

SpaceX launched their historic IPO on June 12, 2026, the largest in history with the company’s valuation surpassing $2 trillion. In their wake, it is tempting to believe that some trees can really grow all the way to space.

The history of the market delivers a consistent reminder: neither trees nor stocks grow to the sky or to space. Assumptions of infinite growth within our finite reality have proven costly time and again. The popular backward-looking CAPE ratio currently sits near 42. Levels this high are typically associated with lower average future returns for equities. Forward Earnings multiple charts show similar levels of historic highs.

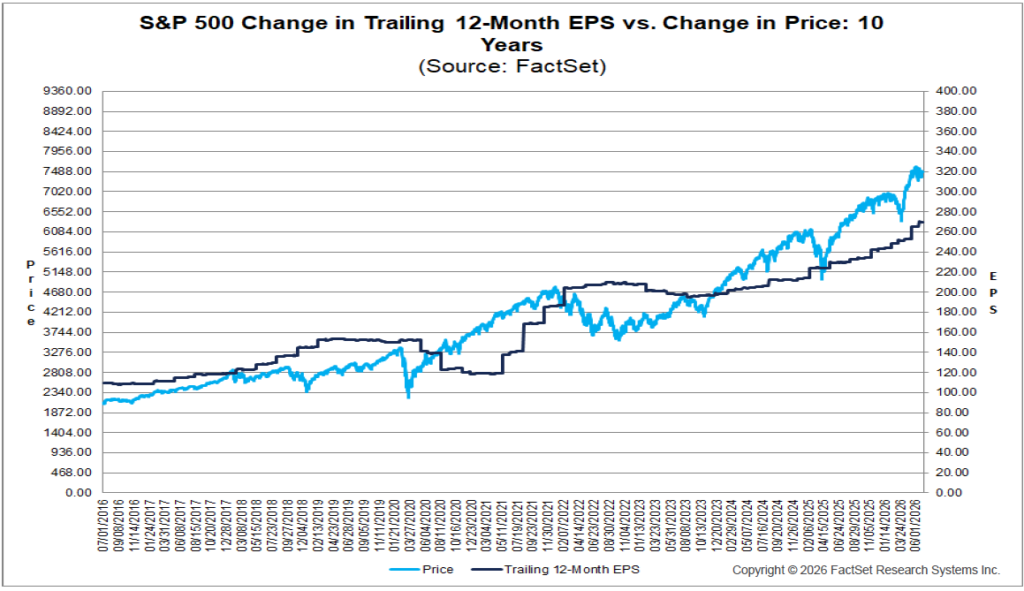

Bulls argue that this time is different. They contend that AI-driven earnings growth has and will continue to justify valuations. Bears counter that return to normal is inevitable and that the higher the peak, the steeper the potential decline. The chart below demonstrates how stock prices for the S&P 500 have grown compared to the actual company earnings behind them over time.

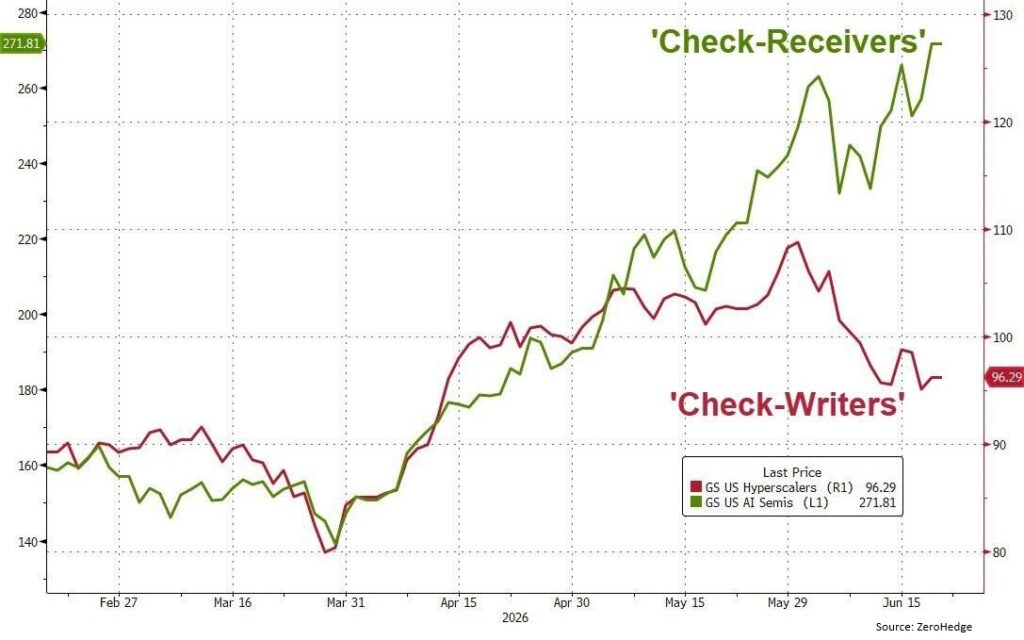

A critical question is whether corporate earnings, particularly within the AI ecosystem, can grow fast enough to validate current prices. Currently, the answer is increasingly split in two. The chart on the next page captures a clear difference: Check-Receivers (primarily AI chip makers) have continued powering higher, while Check-Writers (the largest companies footing the multi-hundred-billion-dollar bill) have shown relative weakness in recent months.

The “picks and shovels” suppliers capture disproportionate early profits. Meanwhile the heavy spenders face margin pressure, over-building fears, and the reality that meaningful return on investment takes time to materialize at scale. AI-related spending for 2026 remains elevated, with estimates in the $500 to $700 billion-plus range across major players. Growth rates in spending are already decelerating in places, and power availability is emerging as a hard constraint.

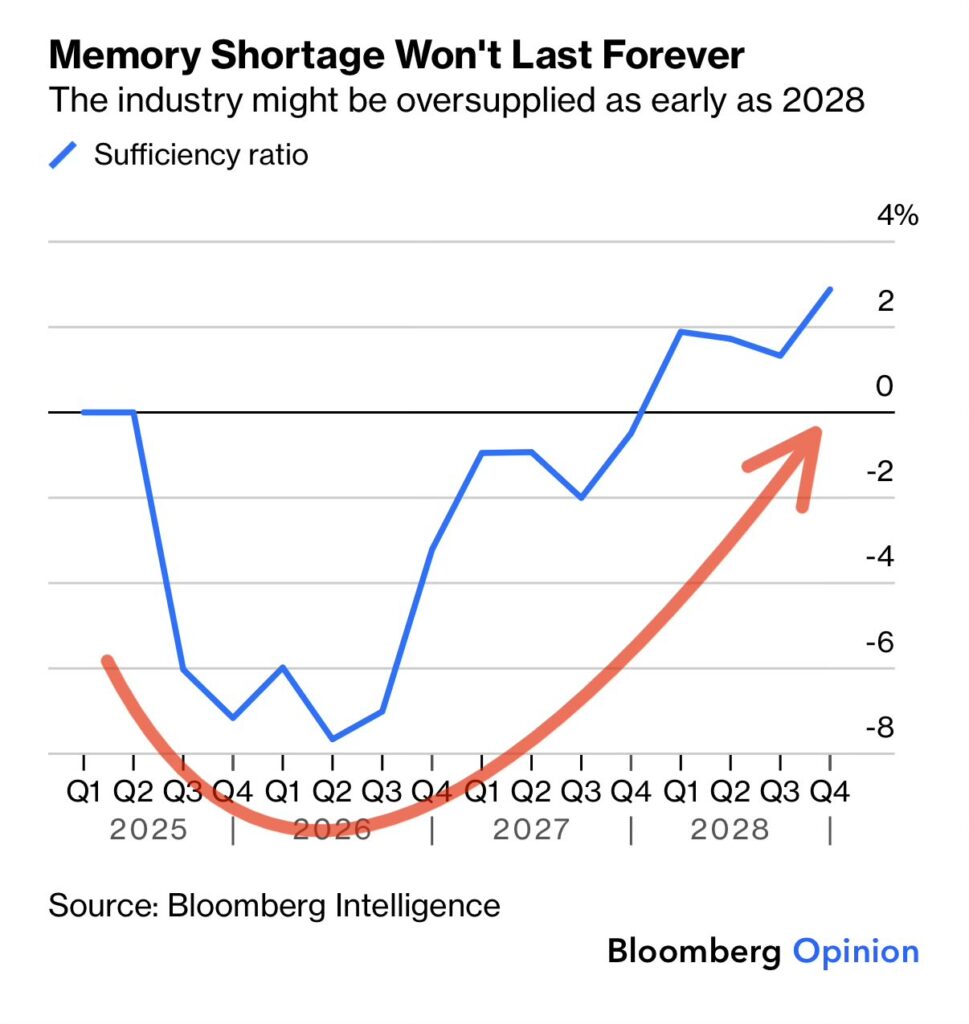

The AI buildout has created one of the strongest memory and semiconductor cycles in history. Memory demand has tightened supply for conventional chips and driven dramatic price increases. Suppliers are effectively sold out through 2026 and 2027 in many segments. Cycles have peaks and valleys. The Bloomberg Intelligence chart below demonstrates the supply and demand balance for memory turning decisively higher as new factories are slated to start production starting late 2027 into 2028. If AI demand growth moderates even modestly, or if power and infrastructure bottlenecks bite harder, the industry could shift from shortage to balanced or outright oversupplied faster than consensus expects.

We are not calling an imminent bust. The structural tailwinds from AI are powerful and multi-year. The rate of change in the cycle is susceptible to slowing down, however, and investors assuming that shortages and high prices last forever may be disappointed. The big three memory makers (Samsung, SK Hynix, Micron) are tightening their spending discipline. History has shown that every memory supercycle eventually normalizes, often abruptly.

Broader Market Backdrop: Rates, Housing and Labor

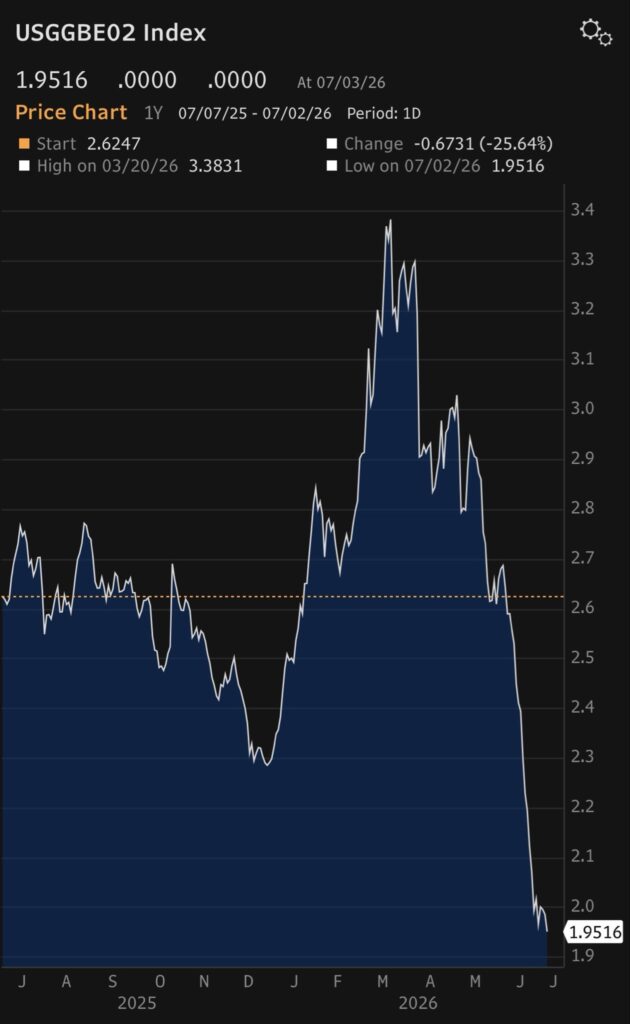

Inflation expectations, and their impacts on interest rates, have exhibited significant volatility. Recent moves reflect evolving expectations around the timing and extent of any Fed easing or potential hiking. In the latest Fed communication, the new Federal Reserve Chair, Kevin Warsh, used firm language to promise price stability. Investors now expect fewer interest rate cuts than earlier anticipated, and even the possibility of an increase. Inflation expectations, increased due to the conflict in the Middle East, have normalized due to calming hostilities and rate hawkishness. The chart on the right shows expected future inflation by comparing regular Treasury bonds with special inflation-protected bonds.

Housing and Demographics. The median age of U.S. homebuyers has continued its steady climb. First-time buyers now approach a median age of 40, while repeat buyers are typically in their late 50s to early 60s. This is more than a demographic curiosity. It signals persistent affordability challenges, high mortgage rates locking in existing homeowners, and delayed wealth-building for younger generations. The long-term implications for consumption, family formation, and the political economy are profound. A record peak in 630,000 more sellers than buyers in March has narrowed slightly in recent months but remains a concern.

Labor Market. The classic unemployment rate recently stopped its slow march upwards, a stabilizing sign for the economy and markets. However, the change in the labor force participation rate shows recent softening after the post-pandemic recovery. While this alone does not signal an upcoming recession, employment softness is a sign of stress which should be monitored closely.

Risk Management in the Later Innings

SpaceX’s achievement is extraordinary and deserves celebration. It demonstrates what focused execution, capital allocation, and technological ambition can accomplish. The company’s public market debut also serves as a timely reminder. Even the most successful ventures trade at valuations that embed heroic assumptions about future growth. Post-IPO moderation in the stock price is a healthy reminder that gravity eventually applies.

Across the broader market we see several factors:

- Valuations at levels that have historically delivered poor forward returns.

- AI earnings leadership concentrated in a handful of enablers while spenders face ROI scrutiny.

- Hardware and memory cycle still strong but with clear visibility to capacity-driven normalization by 2028.

- Policy rates volatile and continued inflation uncertainty.

- Real economy signals (housing affordability, labor participation) showing strain.

We remain constructive on the long-term transformative power of AI and related technologies. We advocate heightened risk awareness in portfolio construction. This includes maintaining discipline on valuation, favoring quality companies with durable strategic advantages and reasonable entry points, diversifying as much as reasonable, and stress-testing for scenarios of slowing growth and/or falling valuations.

Trees do not grow into space. Markets do not either. The investors who thrive over full cycles are those who recognize when the canopy is getting thin and position themselves to act accordingly.

In 2002, Equitas Capital Advisors, LLC was established as a unique company that blends the resources of a large global corporation with the flexibility of a small boutique firm. The registered service mark of Equitas Capital Advisors is Engineering Financial Solutions®and the purpose of Equitas is to design, build, and deliver investment solutions to meet the goals and objectives of our investors. Equitas Capital Advisors, LLC located in New Orleans, has over 200 years of combined investment management consulting experience providing professional investment management services to investors such as foundations, endowments, insurance companies, oil companies, universities, corporate retirement plans, and high net worth family offices.

Disclosures and Disclaimers:

Above information is for illustrative purposes only and has been obtained from reliable sources but no guarantee is made with regard to accuracy or completeness. This information including any specific securities mentioned is for educational, entertainment and illustrative purposes only and not a recommendation or solicitation to purchase or sell any individual security. You cannot invest directly in an index.

Equitas Capital Advisors, LLC is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the advisor has attained a particular level of skill or ability.

Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author on the date of publication and are subject to change. This publication does not involve the rendering of personalized investment advice.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment or strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor. Charts and references to returns do not represent the performance achieved by Equitas Capital Advisors, LLC, or any of its clients.

Asset allocation and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment losses. All investment strategies have the potential for profit or loss. There can be no assurances that an investor’s portfolio will match or outperform any particular benchmark.